mirror of

https://github.com/freqtrade/freqtrade.git

synced 2024-11-10 10:21:59 +00:00

Merge branch 'develop' into pr/SmartManoj/6859

This commit is contained in:

commit

8bf0bf10c5

41

.github/workflows/ci.yml

vendored

41

.github/workflows/ci.yml

vendored

|

|

@ -13,6 +13,10 @@ on:

|

||||||

schedule:

|

schedule:

|

||||||

- cron: '0 5 * * 4'

|

- cron: '0 5 * * 4'

|

||||||

|

|

||||||

|

concurrency:

|

||||||

|

group: ${{ github.workflow }}-${{ github.ref }}

|

||||||

|

cancel-in-progress: true

|

||||||

|

|

||||||

jobs:

|

jobs:

|

||||||

build_linux:

|

build_linux:

|

||||||

|

|

||||||

|

|

@ -26,7 +30,7 @@ jobs:

|

||||||

- uses: actions/checkout@v3

|

- uses: actions/checkout@v3

|

||||||

|

|

||||||

- name: Set up Python

|

- name: Set up Python

|

||||||

uses: actions/setup-python@v3

|

uses: actions/setup-python@v4

|

||||||

with:

|

with:

|

||||||

python-version: ${{ matrix.python-version }}

|

python-version: ${{ matrix.python-version }}

|

||||||

|

|

||||||

|

|

@ -62,12 +66,12 @@ jobs:

|

||||||

- name: Tests

|

- name: Tests

|

||||||

run: |

|

run: |

|

||||||

pytest --random-order --cov=freqtrade --cov-config=.coveragerc

|

pytest --random-order --cov=freqtrade --cov-config=.coveragerc

|

||||||

if: matrix.python-version != '3.9'

|

if: matrix.python-version != '3.9' || matrix.os != 'ubuntu-22.04'

|

||||||

|

|

||||||

- name: Tests incl. ccxt compatibility tests

|

- name: Tests incl. ccxt compatibility tests

|

||||||

run: |

|

run: |

|

||||||

pytest --random-order --cov=freqtrade --cov-config=.coveragerc --longrun

|

pytest --random-order --cov=freqtrade --cov-config=.coveragerc --longrun

|

||||||

if: matrix.python-version == '3.9'

|

if: matrix.python-version == '3.9' && matrix.os == 'ubuntu-22.04'

|

||||||

|

|

||||||

- name: Coveralls

|

- name: Coveralls

|

||||||

if: (runner.os == 'Linux' && matrix.python-version == '3.9')

|

if: (runner.os == 'Linux' && matrix.python-version == '3.9')

|

||||||

|

|

@ -78,11 +82,13 @@ jobs:

|

||||||

# Allow failure for coveralls

|

# Allow failure for coveralls

|

||||||

coveralls || true

|

coveralls || true

|

||||||

|

|

||||||

- name: Backtesting

|

- name: Backtesting (multi)

|

||||||

run: |

|

run: |

|

||||||

cp config_examples/config_bittrex.example.json config.json

|

cp config_examples/config_bittrex.example.json config.json

|

||||||

freqtrade create-userdir --userdir user_data

|

freqtrade create-userdir --userdir user_data

|

||||||

freqtrade backtesting --datadir tests/testdata --strategy SampleStrategy

|

freqtrade new-strategy -s AwesomeStrategy

|

||||||

|

freqtrade new-strategy -s AwesomeStrategyMin --template minimal

|

||||||

|

freqtrade backtesting --datadir tests/testdata --strategy-list AwesomeStrategy AwesomeStrategyMin -i 5m

|

||||||

|

|

||||||

- name: Hyperopt

|

- name: Hyperopt

|

||||||

run: |

|

run: |

|

||||||

|

|

@ -121,7 +127,7 @@ jobs:

|

||||||

- uses: actions/checkout@v3

|

- uses: actions/checkout@v3

|

||||||

|

|

||||||

- name: Set up Python

|

- name: Set up Python

|

||||||

uses: actions/setup-python@v3

|

uses: actions/setup-python@v4

|

||||||

with:

|

with:

|

||||||

python-version: ${{ matrix.python-version }}

|

python-version: ${{ matrix.python-version }}

|

||||||

|

|

||||||

|

|

@ -164,7 +170,8 @@ jobs:

|

||||||

run: |

|

run: |

|

||||||

cp config_examples/config_bittrex.example.json config.json

|

cp config_examples/config_bittrex.example.json config.json

|

||||||

freqtrade create-userdir --userdir user_data

|

freqtrade create-userdir --userdir user_data

|

||||||

freqtrade backtesting --datadir tests/testdata --strategy SampleStrategy

|

freqtrade new-strategy -s AwesomeStrategyAdv --template advanced

|

||||||

|

freqtrade backtesting --datadir tests/testdata --strategy AwesomeStrategyAdv

|

||||||

|

|

||||||

- name: Hyperopt

|

- name: Hyperopt

|

||||||

run: |

|

run: |

|

||||||

|

|

@ -204,7 +211,7 @@ jobs:

|

||||||

- uses: actions/checkout@v3

|

- uses: actions/checkout@v3

|

||||||

|

|

||||||

- name: Set up Python

|

- name: Set up Python

|

||||||

uses: actions/setup-python@v3

|

uses: actions/setup-python@v4

|

||||||

with:

|

with:

|

||||||

python-version: ${{ matrix.python-version }}

|

python-version: ${{ matrix.python-version }}

|

||||||

|

|

||||||

|

|

@ -256,7 +263,7 @@ jobs:

|

||||||

- uses: actions/checkout@v3

|

- uses: actions/checkout@v3

|

||||||

|

|

||||||

- name: Set up Python

|

- name: Set up Python

|

||||||

uses: actions/setup-python@v3

|

uses: actions/setup-python@v4

|

||||||

with:

|

with:

|

||||||

python-version: "3.10"

|

python-version: "3.10"

|

||||||

|

|

||||||

|

|

@ -275,7 +282,7 @@ jobs:

|

||||||

./tests/test_docs.sh

|

./tests/test_docs.sh

|

||||||

|

|

||||||

- name: Set up Python

|

- name: Set up Python

|

||||||

uses: actions/setup-python@v3

|

uses: actions/setup-python@v4

|

||||||

with:

|

with:

|

||||||

python-version: "3.10"

|

python-version: "3.10"

|

||||||

|

|

||||||

|

|

@ -293,18 +300,6 @@ jobs:

|

||||||

details: Freqtrade doc test failed!

|

details: Freqtrade doc test failed!

|

||||||

webhookUrl: ${{ secrets.DISCORD_WEBHOOK }}

|

webhookUrl: ${{ secrets.DISCORD_WEBHOOK }}

|

||||||

|

|

||||||

cleanup-prior-runs:

|

|

||||||

permissions:

|

|

||||||

actions: write # for rokroskar/workflow-run-cleanup-action to obtain workflow name & cancel it

|

|

||||||

contents: read # for rokroskar/workflow-run-cleanup-action to obtain branch

|

|

||||||

runs-on: ubuntu-20.04

|

|

||||||

steps:

|

|

||||||

- name: Cleanup previous runs on this branch

|

|

||||||

uses: rokroskar/workflow-run-cleanup-action@v0.3.3

|

|

||||||

if: "!startsWith(github.ref, 'refs/tags/') && github.ref != 'refs/heads/stable' && github.repository == 'freqtrade/freqtrade'"

|

|

||||||

env:

|

|

||||||

GITHUB_TOKEN: "${{ secrets.GITHUB_TOKEN }}"

|

|

||||||

|

|

||||||

# Notify only once - when CI completes (and after deploy) in case it's successfull

|

# Notify only once - when CI completes (and after deploy) in case it's successfull

|

||||||

notify-complete:

|

notify-complete:

|

||||||

needs: [ build_linux, build_macos, build_windows, docs_check, mypy_version_check ]

|

needs: [ build_linux, build_macos, build_windows, docs_check, mypy_version_check ]

|

||||||

|

|

@ -341,7 +336,7 @@ jobs:

|

||||||

- uses: actions/checkout@v3

|

- uses: actions/checkout@v3

|

||||||

|

|

||||||

- name: Set up Python

|

- name: Set up Python

|

||||||

uses: actions/setup-python@v3

|

uses: actions/setup-python@v4

|

||||||

with:

|

with:

|

||||||

python-version: "3.9"

|

python-version: "3.9"

|

||||||

|

|

||||||

|

|

|

||||||

|

|

@ -13,11 +13,11 @@ repos:

|

||||||

- id: mypy

|

- id: mypy

|

||||||

exclude: build_helpers

|

exclude: build_helpers

|

||||||

additional_dependencies:

|

additional_dependencies:

|

||||||

- types-cachetools==5.0.1

|

- types-cachetools==5.0.2

|

||||||

- types-filelock==3.2.5

|

- types-filelock==3.2.7

|

||||||

- types-requests==2.27.25

|

- types-requests==2.27.30

|

||||||

- types-tabulate==0.8.9

|

- types-tabulate==0.8.9

|

||||||

- types-python-dateutil==2.8.15

|

- types-python-dateutil==2.8.17

|

||||||

# stages: [push]

|

# stages: [push]

|

||||||

|

|

||||||

- repo: https://github.com/pycqa/isort

|

- repo: https://github.com/pycqa/isort

|

||||||

|

|

|

||||||

|

|

@ -1,4 +1,4 @@

|

||||||

FROM python:3.10.4-slim-bullseye as base

|

FROM python:3.10.5-slim-bullseye as base

|

||||||

|

|

||||||

# Setup env

|

# Setup env

|

||||||

ENV LANG C.UTF-8

|

ENV LANG C.UTF-8

|

||||||

|

|

|

||||||

|

|

@ -9,10 +9,6 @@ Freqtrade is a free and open source crypto trading bot written in Python. It is

|

||||||

|

|

||||||

|

|

||||||

|

|

||||||

## Sponsored promotion

|

|

||||||

|

|

||||||

[](https://tokenbot.com/?utm_source=github&utm_medium=freqtrade&utm_campaign=algodevs)

|

|

||||||

|

|

||||||

## Disclaimer

|

## Disclaimer

|

||||||

|

|

||||||

This software is for educational purposes only. Do not risk money which

|

This software is for educational purposes only. Do not risk money which

|

||||||

|

|

@ -39,7 +35,7 @@ Please read the [exchange specific notes](docs/exchanges.md) to learn about even

|

||||||

- [X] [OKX](https://okx.com/) (Former OKEX)

|

- [X] [OKX](https://okx.com/) (Former OKEX)

|

||||||

- [ ] [potentially many others](https://github.com/ccxt/ccxt/). _(We cannot guarantee they will work)_

|

- [ ] [potentially many others](https://github.com/ccxt/ccxt/). _(We cannot guarantee they will work)_

|

||||||

|

|

||||||

### Experimentally, freqtrade also supports futures on the following exchanges

|

### Supported Futures Exchanges (experimental)

|

||||||

|

|

||||||

- [X] [Binance](https://www.binance.com/)

|

- [X] [Binance](https://www.binance.com/)

|

||||||

- [X] [Gate.io](https://www.gate.io/ref/6266643)

|

- [X] [Gate.io](https://www.gate.io/ref/6266643)

|

||||||

|

|

|

||||||

|

|

@ -7,4 +7,5 @@ FROM freqtradeorg/freqtrade:develop

|

||||||

# The below dependency - pyti - serves as an example. Please use whatever you need!

|

# The below dependency - pyti - serves as an example. Please use whatever you need!

|

||||||

RUN pip install --user pyti

|

RUN pip install --user pyti

|

||||||

|

|

||||||

|

# Switch back to user (only if you required root above)

|

||||||

# USER ftuser

|

# USER ftuser

|

||||||

|

|

|

||||||

|

|

@ -22,50 +22,79 @@ DataFrame of the candles that resulted in buy signals. Depending on how many buy

|

||||||

makes, this file may get quite large, so periodically check your `user_data/backtest_results`

|

makes, this file may get quite large, so periodically check your `user_data/backtest_results`

|

||||||

folder to delete old exports.

|

folder to delete old exports.

|

||||||

|

|

||||||

To analyze the buy tags, we need to use the `buy_reasons.py` script from

|

|

||||||

[froggleston's repo](https://github.com/froggleston/freqtrade-buyreasons). Follow the instructions

|

|

||||||

in their README to copy the script into your `freqtrade/scripts/` folder.

|

|

||||||

|

|

||||||

Before running your next backtest, make sure you either delete your old backtest results or run

|

Before running your next backtest, make sure you either delete your old backtest results or run

|

||||||

backtesting with the `--cache none` option to make sure no cached results are used.

|

backtesting with the `--cache none` option to make sure no cached results are used.

|

||||||

|

|

||||||

If all goes well, you should now see a `backtest-result-{timestamp}_signals.pkl` file in the

|

If all goes well, you should now see a `backtest-result-{timestamp}_signals.pkl` file in the

|

||||||

`user_data/backtest_results` folder.

|

`user_data/backtest_results` folder.

|

||||||

|

|

||||||

Now run the `buy_reasons.py` script, supplying a few options:

|

To analyze the entry/exit tags, we now need to use the `freqtrade backtesting-analysis` command

|

||||||

|

with `--analysis-groups` option provided with space-separated arguments (default `0 1 2`):

|

||||||

|

|

||||||

``` bash

|

``` bash

|

||||||

python3 scripts/buy_reasons.py -c <config.json> -s <strategy_name> -t <timerange> -g0,1,2,3,4

|

freqtrade backtesting-analysis -c <config.json> --analysis-groups 0 1 2 3 4

|

||||||

```

|

```

|

||||||

|

|

||||||

The `-g` option is used to specify the various tabular outputs, ranging from the simplest (0)

|

This command will read from the last backtesting results. The `--analysis-groups` option is

|

||||||

to the most detailed per pair, per buy and per sell tag (4). More options are available by

|

used to specify the various tabular outputs showing the profit fo each group or trade,

|

||||||

running with the `-h` option.

|

ranging from the simplest (0) to the most detailed per pair, per buy and per sell tag (4):

|

||||||

|

|

||||||

|

* 1: profit summaries grouped by enter_tag

|

||||||

|

* 2: profit summaries grouped by enter_tag and exit_tag

|

||||||

|

* 3: profit summaries grouped by pair and enter_tag

|

||||||

|

* 4: profit summaries grouped by pair, enter_ and exit_tag (this can get quite large)

|

||||||

|

|

||||||

|

More options are available by running with the `-h` option.

|

||||||

|

|

||||||

|

### Using export-filename

|

||||||

|

|

||||||

|

Normally, `backtesting-analysis` uses the latest backtest results, but if you wanted to go

|

||||||

|

back to a previous backtest output, you need to supply the `--export-filename` option.

|

||||||

|

You can supply the same parameter to `backtest-analysis` with the name of the final backtest

|

||||||

|

output file. This allows you to keep historical versions of backtest results and re-analyse

|

||||||

|

them at a later date:

|

||||||

|

|

||||||

|

``` bash

|

||||||

|

freqtrade backtesting -c <config.json> --timeframe <tf> --strategy <strategy_name> --timerange=<timerange> --export=signals --export-filename=/tmp/mystrat_backtest.json

|

||||||

|

```

|

||||||

|

|

||||||

|

You should see some output similar to below in the logs with the name of the timestamped

|

||||||

|

filename that was exported:

|

||||||

|

|

||||||

|

```

|

||||||

|

2022-06-14 16:28:32,698 - freqtrade.misc - INFO - dumping json to "/tmp/mystrat_backtest-2022-06-14_16-28-32.json"

|

||||||

|

```

|

||||||

|

|

||||||

|

You can then use that filename in `backtesting-analysis`:

|

||||||

|

|

||||||

|

```

|

||||||

|

freqtrade backtesting-analysis -c <config.json> --export-filename=/tmp/mystrat_backtest-2022-06-14_16-28-32.json

|

||||||

|

```

|

||||||

|

|

||||||

### Tuning the buy tags and sell tags to display

|

### Tuning the buy tags and sell tags to display

|

||||||

|

|

||||||

To show only certain buy and sell tags in the displayed output, use the following two options:

|

To show only certain buy and sell tags in the displayed output, use the following two options:

|

||||||

|

|

||||||

```

|

```

|

||||||

--enter_reason_list : Comma separated list of enter signals to analyse. Default: "all"

|

--enter-reason-list : Space-separated list of enter signals to analyse. Default: "all"

|

||||||

--exit_reason_list : Comma separated list of exit signals to analyse. Default: "stop_loss,trailing_stop_loss"

|

--exit-reason-list : Space-separated list of exit signals to analyse. Default: "all"

|

||||||

```

|

```

|

||||||

|

|

||||||

For example:

|

For example:

|

||||||

|

|

||||||

```bash

|

```bash

|

||||||

python3 scripts/buy_reasons.py -c <config.json> -s <strategy_name> -t <timerange> -g0,1,2,3,4 --enter_reason_list "enter_tag_a,enter_tag_b" --exit_reason_list "roi,custom_exit_tag_a,stop_loss"

|

freqtrade backtesting-analysis -c <config.json> --analysis-groups 0 2 --enter-reason-list enter_tag_a enter_tag_b --exit-reason-list roi custom_exit_tag_a stop_loss

|

||||||

```

|

```

|

||||||

|

|

||||||

### Outputting signal candle indicators

|

### Outputting signal candle indicators

|

||||||

|

|

||||||

The real power of the buy_reasons.py script comes from the ability to print out the indicator

|

The real power of `freqtrade backtesting-analysis` comes from the ability to print out the indicator

|

||||||

values present on signal candles to allow fine-grained investigation and tuning of buy signal

|

values present on signal candles to allow fine-grained investigation and tuning of buy signal

|

||||||

indicators. To print out a column for a given set of indicators, use the `--indicator-list`

|

indicators. To print out a column for a given set of indicators, use the `--indicator-list`

|

||||||

option:

|

option:

|

||||||

|

|

||||||

```bash

|

```bash

|

||||||

python3 scripts/buy_reasons.py -c <config.json> -s <strategy_name> -t <timerange> -g0,1,2,3,4 --enter_reason_list "enter_tag_a,enter_tag_b" --exit_reason_list "roi,custom_exit_tag_a,stop_loss" --indicator_list "rsi,rsi_1h,bb_lowerband,ema_9,macd,macdsignal"

|

freqtrade backtesting-analysis -c <config.json> --analysis-groups 0 2 --enter-reason-list enter_tag_a enter_tag_b --exit-reason-list roi custom_exit_tag_a stop_loss --indicator-list rsi rsi_1h bb_lowerband ema_9 macd macdsignal

|

||||||

```

|

```

|

||||||

|

|

||||||

The indicators have to be present in your strategy's main DataFrame (either for your main

|

The indicators have to be present in your strategy's main DataFrame (either for your main

|

||||||

|

|

|

||||||

|

|

@ -98,6 +98,23 @@ class MyAwesomeStrategy(IStrategy):

|

||||||

!!! Note

|

!!! Note

|

||||||

All overrides are optional and can be mixed/matched as necessary.

|

All overrides are optional and can be mixed/matched as necessary.

|

||||||

|

|

||||||

|

### Dynamic parameters

|

||||||

|

|

||||||

|

Parameters can also be defined dynamically, but must be available to the instance once the * [`bot_start()` callback](strategy-callbacks.md#bot-start) has been called.

|

||||||

|

|

||||||

|

``` python

|

||||||

|

|

||||||

|

class MyAwesomeStrategy(IStrategy):

|

||||||

|

|

||||||

|

def bot_start(self, **kwargs) -> None:

|

||||||

|

self.buy_adx = IntParameter(20, 30, default=30, optimize=True)

|

||||||

|

|

||||||

|

# ...

|

||||||

|

```

|

||||||

|

|

||||||

|

!!! Warning

|

||||||

|

Parameters created this way will not show up in the `list-strategies` parameter count.

|

||||||

|

|

||||||

### Overriding Base estimator

|

### Overriding Base estimator

|

||||||

|

|

||||||

You can define your own estimator for Hyperopt by implementing `generate_estimator()` in the Hyperopt subclass.

|

You can define your own estimator for Hyperopt by implementing `generate_estimator()` in the Hyperopt subclass.

|

||||||

|

|

|

||||||

BIN

docs/assets/discord_notification.png

Normal file

BIN

docs/assets/discord_notification.png

Normal file

{kind=link}

Binary file not shown.

|

After Width: | Height: | Size: 48 KiB |

|

|

@ -300,6 +300,7 @@ A backtesting result will look like that:

|

||||||

| Absolute profit | 0.00762792 BTC |

|

| Absolute profit | 0.00762792 BTC |

|

||||||

| Total profit % | 76.2% |

|

| Total profit % | 76.2% |

|

||||||

| CAGR % | 460.87% |

|

| CAGR % | 460.87% |

|

||||||

|

| Profit factor | 1.11 |

|

||||||

| Avg. stake amount | 0.001 BTC |

|

| Avg. stake amount | 0.001 BTC |

|

||||||

| Total trade volume | 0.429 BTC |

|

| Total trade volume | 0.429 BTC |

|

||||||

| | |

|

| | |

|

||||||

|

|

@ -399,6 +400,7 @@ It contains some useful key metrics about performance of your strategy on backte

|

||||||

| Absolute profit | 0.00762792 BTC |

|

| Absolute profit | 0.00762792 BTC |

|

||||||

| Total profit % | 76.2% |

|

| Total profit % | 76.2% |

|

||||||

| CAGR % | 460.87% |

|

| CAGR % | 460.87% |

|

||||||

|

| Profit factor | 1.11 |

|

||||||

| Avg. stake amount | 0.001 BTC |

|

| Avg. stake amount | 0.001 BTC |

|

||||||

| Total trade volume | 0.429 BTC |

|

| Total trade volume | 0.429 BTC |

|

||||||

| | |

|

| | |

|

||||||

|

|

@ -444,6 +446,8 @@ It contains some useful key metrics about performance of your strategy on backte

|

||||||

- `Final balance`: Final balance - starting balance + absolute profit.

|

- `Final balance`: Final balance - starting balance + absolute profit.

|

||||||

- `Absolute profit`: Profit made in stake currency.

|

- `Absolute profit`: Profit made in stake currency.

|

||||||

- `Total profit %`: Total profit. Aligned to the `TOTAL` row's `Tot Profit %` from the first table. Calculated as `(End capital − Starting capital) / Starting capital`.

|

- `Total profit %`: Total profit. Aligned to the `TOTAL` row's `Tot Profit %` from the first table. Calculated as `(End capital − Starting capital) / Starting capital`.

|

||||||

|

- `CAGR %`: Compound annual growth rate.

|

||||||

|

- `Profit factor`: profit / loss.

|

||||||

- `Avg. stake amount`: Average stake amount, either `stake_amount` or the average when using dynamic stake amount.

|

- `Avg. stake amount`: Average stake amount, either `stake_amount` or the average when using dynamic stake amount.

|

||||||

- `Total trade volume`: Volume generated on the exchange to reach the above profit.

|

- `Total trade volume`: Volume generated on the exchange to reach the above profit.

|

||||||

- `Best Pair` / `Worst Pair`: Best and worst performing pair, and it's corresponding `Cum Profit %`.

|

- `Best Pair` / `Worst Pair`: Best and worst performing pair, and it's corresponding `Cum Profit %`.

|

||||||

|

|

@ -530,8 +534,9 @@ Since backtesting lacks some detailed information about what happens within a ca

|

||||||

- Exit-reason does not explain if a trade was positive or negative, just what triggered the exit (this can look odd if negative ROI values are used)

|

- Exit-reason does not explain if a trade was positive or negative, just what triggered the exit (this can look odd if negative ROI values are used)

|

||||||

- Evaluation sequence (if multiple signals happen on the same candle)

|

- Evaluation sequence (if multiple signals happen on the same candle)

|

||||||

- Exit-signal

|

- Exit-signal

|

||||||

- ROI (if not stoploss)

|

|

||||||

- Stoploss

|

- Stoploss

|

||||||

|

- ROI

|

||||||

|

- Trailing stoploss

|

||||||

|

|

||||||

Taking these assumptions, backtesting tries to mirror real trading as closely as possible. However, backtesting will **never** replace running a strategy in dry-run mode.

|

Taking these assumptions, backtesting tries to mirror real trading as closely as possible. However, backtesting will **never** replace running a strategy in dry-run mode.

|

||||||

Also, keep in mind that past results don't guarantee future success.

|

Also, keep in mind that past results don't guarantee future success.

|

||||||

|

|

|

||||||

|

|

@ -140,7 +140,7 @@ Mandatory parameters are marked as **Required**, which means that they are requi

|

||||||

| `dry_run` | **Required.** Define if the bot must be in Dry Run or production mode. <br>*Defaults to `true`.* <br> **Datatype:** Boolean

|

| `dry_run` | **Required.** Define if the bot must be in Dry Run or production mode. <br>*Defaults to `true`.* <br> **Datatype:** Boolean

|

||||||

| `dry_run_wallet` | Define the starting amount in stake currency for the simulated wallet used by the bot running in Dry Run mode.<br>*Defaults to `1000`.* <br> **Datatype:** Float

|

| `dry_run_wallet` | Define the starting amount in stake currency for the simulated wallet used by the bot running in Dry Run mode.<br>*Defaults to `1000`.* <br> **Datatype:** Float

|

||||||

| `cancel_open_orders_on_exit` | Cancel open orders when the `/stop` RPC command is issued, `Ctrl+C` is pressed or the bot dies unexpectedly. When set to `true`, this allows you to use `/stop` to cancel unfilled and partially filled orders in the event of a market crash. It does not impact open positions. <br>*Defaults to `false`.* <br> **Datatype:** Boolean

|

| `cancel_open_orders_on_exit` | Cancel open orders when the `/stop` RPC command is issued, `Ctrl+C` is pressed or the bot dies unexpectedly. When set to `true`, this allows you to use `/stop` to cancel unfilled and partially filled orders in the event of a market crash. It does not impact open positions. <br>*Defaults to `false`.* <br> **Datatype:** Boolean

|

||||||

| `process_only_new_candles` | Enable processing of indicators only when new candles arrive. If false each loop populates the indicators, this will mean the same candle is processed many times creating system load but can be useful of your strategy depends on tick data not only candle. [Strategy Override](#parameters-in-the-strategy). <br>*Defaults to `false`.* <br> **Datatype:** Boolean

|

| `process_only_new_candles` | Enable processing of indicators only when new candles arrive. If false each loop populates the indicators, this will mean the same candle is processed many times creating system load but can be useful of your strategy depends on tick data not only candle. [Strategy Override](#parameters-in-the-strategy). <br>*Defaults to `true`.* <br> **Datatype:** Boolean

|

||||||

| `minimal_roi` | **Required.** Set the threshold as ratio the bot will use to exit a trade. [More information below](#understand-minimal_roi). [Strategy Override](#parameters-in-the-strategy). <br> **Datatype:** Dict

|

| `minimal_roi` | **Required.** Set the threshold as ratio the bot will use to exit a trade. [More information below](#understand-minimal_roi). [Strategy Override](#parameters-in-the-strategy). <br> **Datatype:** Dict

|

||||||

| `stoploss` | **Required.** Value as ratio of the stoploss used by the bot. More details in the [stoploss documentation](stoploss.md). [Strategy Override](#parameters-in-the-strategy). <br> **Datatype:** Float (as ratio)

|

| `stoploss` | **Required.** Value as ratio of the stoploss used by the bot. More details in the [stoploss documentation](stoploss.md). [Strategy Override](#parameters-in-the-strategy). <br> **Datatype:** Float (as ratio)

|

||||||

| `trailing_stop` | Enables trailing stoploss (based on `stoploss` in either configuration or strategy file). More details in the [stoploss documentation](stoploss.md#trailing-stop-loss). [Strategy Override](#parameters-in-the-strategy). <br> **Datatype:** Boolean

|

| `trailing_stop` | Enables trailing stoploss (based on `stoploss` in either configuration or strategy file). More details in the [stoploss documentation](stoploss.md#trailing-stop-loss). [Strategy Override](#parameters-in-the-strategy). <br> **Datatype:** Boolean

|

||||||

|

|

@ -230,6 +230,7 @@ Mandatory parameters are marked as **Required**, which means that they are requi

|

||||||

| `dataformat_trades` | Data format to use to store historical trades data. <br> *Defaults to `jsongz`*. <br> **Datatype:** String

|

| `dataformat_trades` | Data format to use to store historical trades data. <br> *Defaults to `jsongz`*. <br> **Datatype:** String

|

||||||

| `position_adjustment_enable` | Enables the strategy to use position adjustments (additional buys or sells). [More information here](strategy-callbacks.md#adjust-trade-position). <br> [Strategy Override](#parameters-in-the-strategy). <br>*Defaults to `false`.*<br> **Datatype:** Boolean

|

| `position_adjustment_enable` | Enables the strategy to use position adjustments (additional buys or sells). [More information here](strategy-callbacks.md#adjust-trade-position). <br> [Strategy Override](#parameters-in-the-strategy). <br>*Defaults to `false`.*<br> **Datatype:** Boolean

|

||||||

| `max_entry_position_adjustment` | Maximum additional order(s) for each open trade on top of the first entry Order. Set it to `-1` for unlimited additional orders. [More information here](strategy-callbacks.md#adjust-trade-position). <br> [Strategy Override](#parameters-in-the-strategy). <br>*Defaults to `-1`.*<br> **Datatype:** Positive Integer or -1

|

| `max_entry_position_adjustment` | Maximum additional order(s) for each open trade on top of the first entry Order. Set it to `-1` for unlimited additional orders. [More information here](strategy-callbacks.md#adjust-trade-position). <br> [Strategy Override](#parameters-in-the-strategy). <br>*Defaults to `-1`.*<br> **Datatype:** Positive Integer or -1

|

||||||

|

| `futures_funding_rate` | User-specified funding rate to be used when historical funding rates are not available from the exchange. This does not overwrite real historical rates. It is recommended that this be set to 0 unless you are testing a specific coin and you understand how the funding rate will affect freqtrade's profit calculations. [More information here](leverage.md#unavailable-funding-rates) <br>*Defaults to None.*<br> **Datatype:** Float

|

||||||

|

|

||||||

### Parameters in the strategy

|

### Parameters in the strategy

|

||||||

|

|

||||||

|

|

@ -583,7 +584,7 @@ Once you will be happy with your bot performance running in the Dry-run mode, yo

|

||||||

* Market orders fill based on orderbook volume the moment the order is placed.

|

* Market orders fill based on orderbook volume the moment the order is placed.

|

||||||

* Limit orders fill once the price reaches the defined level - or time out based on `unfilledtimeout` settings.

|

* Limit orders fill once the price reaches the defined level - or time out based on `unfilledtimeout` settings.

|

||||||

* In combination with `stoploss_on_exchange`, the stop_loss price is assumed to be filled.

|

* In combination with `stoploss_on_exchange`, the stop_loss price is assumed to be filled.

|

||||||

* Open orders (not trades, which are stored in the database) are reset on bot restart.

|

* Open orders (not trades, which are stored in the database) are kept open after bot restarts, with the assumption that they were not filled while being offline.

|

||||||

|

|

||||||

## Switch to production mode

|

## Switch to production mode

|

||||||

|

|

||||||

|

|

|

||||||

|

|

@ -314,6 +314,32 @@ The output will show the last entry from the Exchange as well as the current UTC

|

||||||

If the day shows the same day, then the last candle can be assumed as incomplete and should be dropped (leave the setting `"ohlcv_partial_candle"` from the exchange-class untouched / True). Otherwise, set `"ohlcv_partial_candle"` to `False` to not drop Candles (shown in the example above).

|

If the day shows the same day, then the last candle can be assumed as incomplete and should be dropped (leave the setting `"ohlcv_partial_candle"` from the exchange-class untouched / True). Otherwise, set `"ohlcv_partial_candle"` to `False` to not drop Candles (shown in the example above).

|

||||||

Another way is to run this command multiple times in a row and observe if the volume is changing (while the date remains the same).

|

Another way is to run this command multiple times in a row and observe if the volume is changing (while the date remains the same).

|

||||||

|

|

||||||

|

### Update binance cached leverage tiers

|

||||||

|

|

||||||

|

Updating leveraged tiers should be done regularly - and requires an authenticated account with futures enabled.

|

||||||

|

|

||||||

|

``` python

|

||||||

|

import ccxt

|

||||||

|

import json

|

||||||

|

from pathlib import Path

|

||||||

|

|

||||||

|

exchange = ccxt.binance({

|

||||||

|

'apiKey': '<apikey>',

|

||||||

|

'secret': '<secret>'

|

||||||

|

'options': {'defaultType': 'future'}

|

||||||

|

})

|

||||||

|

_ = exchange.load_markets()

|

||||||

|

|

||||||

|

lev_tiers = exchange.fetch_leverage_tiers()

|

||||||

|

|

||||||

|

# Assumes this is running in the root of the repository.

|

||||||

|

file = Path('freqtrade/exchange/binance_leverage_tiers.json')

|

||||||

|

json.dump(lev_tiers, file.open('w'), indent=2)

|

||||||

|

|

||||||

|

```

|

||||||

|

|

||||||

|

This file should then be contributed upstream, so others can benefit from this, too.

|

||||||

|

|

||||||

## Updating example notebooks

|

## Updating example notebooks

|

||||||

|

|

||||||

To keep the jupyter notebooks aligned with the documentation, the following should be ran after updating a example notebook.

|

To keep the jupyter notebooks aligned with the documentation, the following should be ran after updating a example notebook.

|

||||||

|

|

|

||||||

|

|

@ -680,7 +680,7 @@ class MyAwesomeStrategy(IStrategy):

|

||||||

|

|

||||||

!!! Note

|

!!! Note

|

||||||

Values in the configuration file will overwrite Parameter-file level parameters - and both will overwrite parameters within the strategy.

|

Values in the configuration file will overwrite Parameter-file level parameters - and both will overwrite parameters within the strategy.

|

||||||

The prevalence is therefore: config > parameter file > strategy

|

The prevalence is therefore: config > parameter file > strategy `*_params` > parameter default

|

||||||

|

|

||||||

### Understand Hyperopt ROI results

|

### Understand Hyperopt ROI results

|

||||||

|

|

||||||

|

|

|

||||||

|

|

@ -22,10 +22,6 @@ Freqtrade is a free and open source crypto trading bot written in Python. It is

|

||||||

|

|

||||||

|

|

||||||

|

|

||||||

## Sponsored promotion

|

|

||||||

|

|

||||||

[](https://tokenbot.com/?utm_source=github&utm_medium=freqtrade&utm_campaign=algodevs)

|

|

||||||

|

|

||||||

## Features

|

## Features

|

||||||

|

|

||||||

- Develop your Strategy: Write your strategy in python, using [pandas](https://pandas.pydata.org/). Example strategies to inspire you are available in the [strategy repository](https://github.com/freqtrade/freqtrade-strategies).

|

- Develop your Strategy: Write your strategy in python, using [pandas](https://pandas.pydata.org/). Example strategies to inspire you are available in the [strategy repository](https://github.com/freqtrade/freqtrade-strategies).

|

||||||

|

|

@ -51,7 +47,7 @@ Please read the [exchange specific notes](exchanges.md) to learn about eventual,

|

||||||

- [X] [OKX](https://okx.com/) (Former OKEX)

|

- [X] [OKX](https://okx.com/) (Former OKEX)

|

||||||

- [ ] [potentially many others through <img alt="ccxt" width="30px" src="assets/ccxt-logo.svg" />](https://github.com/ccxt/ccxt/). _(We cannot guarantee they will work)_

|

- [ ] [potentially many others through <img alt="ccxt" width="30px" src="assets/ccxt-logo.svg" />](https://github.com/ccxt/ccxt/). _(We cannot guarantee they will work)_

|

||||||

|

|

||||||

### Experimentally, freqtrade also supports futures on the following exchanges:

|

### Supported Futures Exchanges (experimental)

|

||||||

|

|

||||||

- [X] [Binance](https://www.binance.com/)

|

- [X] [Binance](https://www.binance.com/)

|

||||||

- [X] [Gate.io](https://www.gate.io/ref/6266643)

|

- [X] [Gate.io](https://www.gate.io/ref/6266643)

|

||||||

|

|

|

||||||

|

|

@ -64,7 +64,10 @@ You will also have to pick a "margin mode" (explanation below) - with freqtrade

|

||||||

|

|

||||||

### Margin mode

|

### Margin mode

|

||||||

|

|

||||||

The possible values are: `isolated`, or `cross`(*currently unavailable*)

|

On top of `trading_mode` - you will also have to configure your `margin_mode`.

|

||||||

|

While freqtrade currently only supports one margin mode, this will change, and by configuring it now you're all set for future updates.

|

||||||

|

|

||||||

|

The possible values are: `isolated`, or `cross`(*currently unavailable*).

|

||||||

|

|

||||||

#### Isolated margin mode

|

#### Isolated margin mode

|

||||||

|

|

||||||

|

|

@ -82,6 +85,16 @@ One account is used to share collateral between markets (trading pairs). Margin

|

||||||

"margin_mode": "cross"

|

"margin_mode": "cross"

|

||||||

```

|

```

|

||||||

|

|

||||||

|

## Set leverage to use

|

||||||

|

|

||||||

|

Different strategies and risk profiles will require different levels of leverage.

|

||||||

|

While you could configure one static leverage value - freqtrade offers you the flexibility to adjust this via [strategy leverage callback](strategy-callbacks.md#leverage-callback) - which allows you to use different leverages by pair, or based on some other factor benefitting your strategy result.

|

||||||

|

|

||||||

|

If not implemented, leverage defaults to 1x (no leverage).

|

||||||

|

|

||||||

|

!!! Warning

|

||||||

|

Higher leverage also equals higher risk - be sure you fully understand the implications of using leverage!

|

||||||

|

|

||||||

## Understand `liquidation_buffer`

|

## Understand `liquidation_buffer`

|

||||||

|

|

||||||

*Defaults to `0.05`*

|

*Defaults to `0.05`*

|

||||||

|

|

@ -101,6 +114,13 @@ Possible values are any floats between 0.0 and 0.99

|

||||||

!!! Danger "A `liquidation_buffer` of 0.0, or a low `liquidation_buffer` is likely to result in liquidations, and liquidation fees"

|

!!! Danger "A `liquidation_buffer` of 0.0, or a low `liquidation_buffer` is likely to result in liquidations, and liquidation fees"

|

||||||

Currently Freqtrade is able to calculate liquidation prices, but does not calculate liquidation fees. Setting your `liquidation_buffer` to 0.0, or using a low `liquidation_buffer` could result in your positions being liquidated. Freqtrade does not track liquidation fees, so liquidations will result in inaccurate profit/loss results for your bot. If you use a low `liquidation_buffer`, it is recommended to use `stoploss_on_exchange` if your exchange supports this.

|

Currently Freqtrade is able to calculate liquidation prices, but does not calculate liquidation fees. Setting your `liquidation_buffer` to 0.0, or using a low `liquidation_buffer` could result in your positions being liquidated. Freqtrade does not track liquidation fees, so liquidations will result in inaccurate profit/loss results for your bot. If you use a low `liquidation_buffer`, it is recommended to use `stoploss_on_exchange` if your exchange supports this.

|

||||||

|

|

||||||

|

## Unavailable funding rates

|

||||||

|

|

||||||

|

For futures data, exchanges commonly provide the futures candles, the marks, and the funding rates. However, it is common that whilst candles and marks might be available, the funding rates are not. This can affect backtesting timeranges, i.e. you may only be able to test recent timeranges and not earlier, experiencing the `No data found. Terminating.` error. To get around this, add the `futures_funding_rate` config option as listed in [configuration.md](configuration.md), and it is recommended that you set this to `0`, unless you know a given specific funding rate for your pair, exchange and timerange. Setting this to anything other than `0` can have drastic effects on your profit calculations within strategy, e.g. within the `custom_exit`, `custom_stoploss`, etc functions.

|

||||||

|

|

||||||

|

!!! Warning "This will mean your backtests are inaccurate."

|

||||||

|

This will not overwrite funding rates that are available from the exchange, but bear in mind that setting a false funding rate will mean backtesting results will be inaccurate for historical timeranges where funding rates are not available.

|

||||||

|

|

||||||

### Developer

|

### Developer

|

||||||

|

|

||||||

#### Margin mode

|

#### Margin mode

|

||||||

|

|

|

||||||

|

|

@ -1,5 +1,5 @@

|

||||||

mkdocs==1.3.0

|

mkdocs==1.3.0

|

||||||

mkdocs-material==8.2.15

|

mkdocs-material==8.3.6

|

||||||

mdx_truly_sane_lists==1.2

|

mdx_truly_sane_lists==1.2

|

||||||

pymdown-extensions==9.4

|

pymdown-extensions==9.5

|

||||||

jinja2==3.1.2

|

jinja2==3.1.2

|

||||||

|

|

|

||||||

|

|

@ -89,11 +89,12 @@ WHERE id=31;

|

||||||

|

|

||||||

If you'd still like to remove a trade from the database directly, you can use the below query.

|

If you'd still like to remove a trade from the database directly, you can use the below query.

|

||||||

|

|

||||||

```sql

|

!!! Danger

|

||||||

DELETE FROM trades WHERE id = <tradeid>;

|

Some systems (Ubuntu) disable foreign keys in their sqlite3 packaging. When using sqlite - please ensure that foreign keys are on by running `PRAGMA foreign_keys = ON` before the above query.

|

||||||

```

|

|

||||||

|

|

||||||

```sql

|

```sql

|

||||||

|

DELETE FROM trades WHERE id = <tradeid>;

|

||||||

|

|

||||||

DELETE FROM trades WHERE id = 31;

|

DELETE FROM trades WHERE id = 31;

|

||||||

```

|

```

|

||||||

|

|

||||||

|

|

@ -102,13 +103,20 @@ DELETE FROM trades WHERE id = 31;

|

||||||

|

|

||||||

## Use a different database system

|

## Use a different database system

|

||||||

|

|

||||||

|

Freqtrade is using SQLAlchemy, which supports multiple different database systems. As such, a multitude of database systems should be supported.

|

||||||

|

Freqtrade does not depend or install any additional database driver. Please refer to the [SQLAlchemy docs](https://docs.sqlalchemy.org/en/14/core/engines.html#database-urls) on installation instructions for the respective database systems.

|

||||||

|

|

||||||

|

The following systems have been tested and are known to work with freqtrade:

|

||||||

|

|

||||||

|

* sqlite (default)

|

||||||

|

* PostgreSQL)

|

||||||

|

* MariaDB

|

||||||

|

|

||||||

!!! Warning

|

!!! Warning

|

||||||

By using one of the below database systems, you acknowledge that you know how to manage such a system. Freqtrade will not provide any support with setup or maintenance (or backups) of the below database systems.

|

By using one of the below database systems, you acknowledge that you know how to manage such a system. The freqtrade team will not provide any support with setup or maintenance (or backups) of the below database systems.

|

||||||

|

|

||||||

### PostgreSQL

|

### PostgreSQL

|

||||||

|

|

||||||

Freqtrade supports PostgreSQL by using SQLAlchemy, which supports multiple different database systems.

|

|

||||||

|

|

||||||

Installation:

|

Installation:

|

||||||

`pip install psycopg2-binary`

|

`pip install psycopg2-binary`

|

||||||

|

|

||||||

|

|

|

||||||

|

|

@ -191,6 +191,19 @@ For example, simplified math:

|

||||||

!!! Tip

|

!!! Tip

|

||||||

Make sure to have this value (`trailing_stop_positive_offset`) lower than minimal ROI, otherwise minimal ROI will apply first and sell the trade.

|

Make sure to have this value (`trailing_stop_positive_offset`) lower than minimal ROI, otherwise minimal ROI will apply first and sell the trade.

|

||||||

|

|

||||||

|

## Stoploss and Leverage

|

||||||

|

|

||||||

|

Stoploss should be thought of as "risk on this trade" - so a stoploss of 10% on a 100$ trade means you are willing to lose 10$ (10%) on this trade - which would trigger if the price moves 10% to the downside.

|

||||||

|

|

||||||

|

When using leverage, the same principle is applied - with stoploss defining the risk on the trade (the amount you are willing to lose).

|

||||||

|

|

||||||

|

Therefore, a stoploss of 10% on a 10x trade would trigger on a 1% price move.

|

||||||

|

If your stake amount (own capital) was 100$ - this trade would be 1000$ at 10x (after leverage).

|

||||||

|

If price moves 1% - you've lost 10$ of your own capital - therfore stoploss will trigger in this case.

|

||||||

|

|

||||||

|

Make sure to be aware of this, and avoid using too tight stoploss (at 10x leverage, 10% risk may be too little to allow the trade to "breath" a little).

|

||||||

|

|

||||||

|

|

||||||

## Changing stoploss on open trades

|

## Changing stoploss on open trades

|

||||||

|

|

||||||

A stoploss on an open trade can be changed by changing the value in the configuration or strategy and use the `/reload_config` command (alternatively, completely stopping and restarting the bot also works).

|

A stoploss on an open trade can be changed by changing the value in the configuration or strategy and use the `/reload_config` command (alternatively, completely stopping and restarting the bot also works).

|

||||||

|

|

|

||||||

|

|

@ -46,6 +46,9 @@ class AwesomeStrategy(IStrategy):

|

||||||

self.cust_remote_data = requests.get('https://some_remote_source.example.com')

|

self.cust_remote_data = requests.get('https://some_remote_source.example.com')

|

||||||

|

|

||||||

```

|

```

|

||||||

|

|

||||||

|

During hyperopt, this runs only once at startup.

|

||||||

|

|

||||||

## Bot loop start

|

## Bot loop start

|

||||||

|

|

||||||

A simple callback which is called once at the start of every bot throttling iteration (roughly every 5 seconds, unless configured differently).

|

A simple callback which is called once at the start of every bot throttling iteration (roughly every 5 seconds, unless configured differently).

|

||||||

|

|

@ -546,10 +549,12 @@ class AwesomeStrategy(IStrategy):

|

||||||

|

|

||||||

:param pair: Pair that's about to be bought/shorted.

|

:param pair: Pair that's about to be bought/shorted.

|

||||||

:param order_type: Order type (as configured in order_types). usually limit or market.

|

:param order_type: Order type (as configured in order_types). usually limit or market.

|

||||||

:param amount: Amount in target (quote) currency that's going to be traded.

|

:param amount: Amount in target (base) currency that's going to be traded.

|

||||||

:param rate: Rate that's going to be used when using limit orders

|

:param rate: Rate that's going to be used when using limit orders

|

||||||

|

or current rate for market orders.

|

||||||

:param time_in_force: Time in force. Defaults to GTC (Good-til-cancelled).

|

:param time_in_force: Time in force. Defaults to GTC (Good-til-cancelled).

|

||||||

:param current_time: datetime object, containing the current datetime

|

:param current_time: datetime object, containing the current datetime

|

||||||

|

:param entry_tag: Optional entry_tag (buy_tag) if provided with the buy signal.

|

||||||

:param side: 'long' or 'short' - indicating the direction of the proposed trade

|

:param side: 'long' or 'short' - indicating the direction of the proposed trade

|

||||||

:param **kwargs: Ensure to keep this here so updates to this won't break your strategy.

|

:param **kwargs: Ensure to keep this here so updates to this won't break your strategy.

|

||||||

:return bool: When True is returned, then the buy-order is placed on the exchange.

|

:return bool: When True is returned, then the buy-order is placed on the exchange.

|

||||||

|

|

@ -563,6 +568,14 @@ class AwesomeStrategy(IStrategy):

|

||||||

|

|

||||||

`confirm_trade_exit()` can be used to abort a trade exit (sell) at the latest second (maybe because the price is not what we expect).

|

`confirm_trade_exit()` can be used to abort a trade exit (sell) at the latest second (maybe because the price is not what we expect).

|

||||||

|

|

||||||

|

`confirm_trade_exit()` may be called multiple times within one iteration for the same trade if different exit-reasons apply.

|

||||||

|

The exit-reasons (if applicable) will be in the following sequence:

|

||||||

|

|

||||||

|

* `exit_signal` / `custom_exit`

|

||||||

|

* `stop_loss`

|

||||||

|

* `roi`

|

||||||

|

* `trailing_stop_loss`

|

||||||

|

|

||||||

``` python

|

``` python

|

||||||

from freqtrade.persistence import Trade

|

from freqtrade.persistence import Trade

|

||||||

|

|

||||||

|

|

@ -575,7 +588,7 @@ class AwesomeStrategy(IStrategy):

|

||||||

rate: float, time_in_force: str, exit_reason: str,

|

rate: float, time_in_force: str, exit_reason: str,

|

||||||

current_time: datetime, **kwargs) -> bool:

|

current_time: datetime, **kwargs) -> bool:

|

||||||

"""

|

"""

|

||||||

Called right before placing a regular sell order.

|

Called right before placing a regular exit order.

|

||||||

Timing for this function is critical, so avoid doing heavy computations or

|

Timing for this function is critical, so avoid doing heavy computations or

|

||||||

network requests in this method.

|

network requests in this method.

|

||||||

|

|

||||||

|

|

@ -583,17 +596,19 @@ class AwesomeStrategy(IStrategy):

|

||||||

|

|

||||||

When not implemented by a strategy, returns True (always confirming).

|

When not implemented by a strategy, returns True (always confirming).

|

||||||

|

|

||||||

:param pair: Pair that's about to be sold.

|

:param pair: Pair for trade that's about to be exited.

|

||||||

|

:param trade: trade object.

|

||||||

:param order_type: Order type (as configured in order_types). usually limit or market.

|

:param order_type: Order type (as configured in order_types). usually limit or market.

|

||||||

:param amount: Amount in quote currency.

|

:param amount: Amount in base currency.

|

||||||

:param rate: Rate that's going to be used when using limit orders

|

:param rate: Rate that's going to be used when using limit orders

|

||||||

|

or current rate for market orders.

|

||||||

:param time_in_force: Time in force. Defaults to GTC (Good-til-cancelled).

|

:param time_in_force: Time in force. Defaults to GTC (Good-til-cancelled).

|

||||||

:param exit_reason: Exit reason.

|

:param exit_reason: Exit reason.

|

||||||

Can be any of ['roi', 'stop_loss', 'stoploss_on_exchange', 'trailing_stop_loss',

|

Can be any of ['roi', 'stop_loss', 'stoploss_on_exchange', 'trailing_stop_loss',

|

||||||

'exit_signal', 'force_exit', 'emergency_exit']

|

'exit_signal', 'force_exit', 'emergency_exit']

|

||||||

:param current_time: datetime object, containing the current datetime

|

:param current_time: datetime object, containing the current datetime

|

||||||

:param **kwargs: Ensure to keep this here so updates to this won't break your strategy.

|

:param **kwargs: Ensure to keep this here so updates to this won't break your strategy.

|

||||||

:return bool: When True is returned, then the exit-order is placed on the exchange.

|

:return bool: When True, then the exit-order is placed on the exchange.

|

||||||

False aborts the process

|

False aborts the process

|

||||||

"""

|

"""

|

||||||

if exit_reason == 'force_exit' and trade.calc_profit_ratio(rate) < 0:

|

if exit_reason == 'force_exit' and trade.calc_profit_ratio(rate) < 0:

|

||||||

|

|

@ -605,6 +620,9 @@ class AwesomeStrategy(IStrategy):

|

||||||

|

|

||||||

```

|

```

|

||||||

|

|

||||||

|

!!! Warning

|

||||||

|

`confirm_trade_exit()` can prevent stoploss exits, causing significant losses as this would ignore stoploss exits.

|

||||||

|

|

||||||

## Adjust trade position

|

## Adjust trade position

|

||||||

|

|

||||||

The `position_adjustment_enable` strategy property enables the usage of `adjust_trade_position()` callback in the strategy.

|

The `position_adjustment_enable` strategy property enables the usage of `adjust_trade_position()` callback in the strategy.

|

||||||

|

|

@ -656,7 +674,7 @@ class DigDeeperStrategy(IStrategy):

|

||||||

|

|

||||||

# This is called when placing the initial order (opening trade)

|

# This is called when placing the initial order (opening trade)

|

||||||

def custom_stake_amount(self, pair: str, current_time: datetime, current_rate: float,

|

def custom_stake_amount(self, pair: str, current_time: datetime, current_rate: float,

|

||||||

proposed_stake: float, min_stake: float, max_stake: float,

|

proposed_stake: float, min_stake: Optional[float], max_stake: float,

|

||||||

entry_tag: Optional[str], side: str, **kwargs) -> float:

|

entry_tag: Optional[str], side: str, **kwargs) -> float:

|

||||||

|

|

||||||

# We need to leave most of the funds for possible further DCA orders

|

# We need to leave most of the funds for possible further DCA orders

|

||||||

|

|

@ -664,7 +682,7 @@ class DigDeeperStrategy(IStrategy):

|

||||||

return proposed_stake / self.max_dca_multiplier

|

return proposed_stake / self.max_dca_multiplier

|

||||||

|

|

||||||

def adjust_trade_position(self, trade: Trade, current_time: datetime,

|

def adjust_trade_position(self, trade: Trade, current_time: datetime,

|

||||||

current_rate: float, current_profit: float, min_stake: float,

|

current_rate: float, current_profit: float, min_stake: Optional[float],

|

||||||

max_stake: float, **kwargs):

|

max_stake: float, **kwargs):

|

||||||

"""

|

"""

|

||||||

Custom trade adjustment logic, returning the stake amount that a trade should be increased.

|

Custom trade adjustment logic, returning the stake amount that a trade should be increased.

|

||||||

|

|

@ -788,19 +806,23 @@ For markets / exchanges that don't support leverage, this method is ignored.

|

||||||

|

|

||||||

``` python

|

``` python

|

||||||

class AwesomeStrategy(IStrategy):

|

class AwesomeStrategy(IStrategy):

|

||||||

def leverage(self, pair: str, current_time: 'datetime', current_rate: float,

|

def leverage(self, pair: str, current_time: datetime, current_rate: float,

|

||||||

proposed_leverage: float, max_leverage: float, side: str,

|

proposed_leverage: float, max_leverage: float, entry_tag: Optional[str], side: str,

|

||||||

**kwargs) -> float:

|

**kwargs) -> float:

|

||||||

"""

|

"""

|

||||||

Customize leverage for each new trade.

|

Customize leverage for each new trade. This method is only called in futures mode.

|

||||||

|

|

||||||

:param pair: Pair that's currently analyzed

|

:param pair: Pair that's currently analyzed

|

||||||

:param current_time: datetime object, containing the current datetime

|

:param current_time: datetime object, containing the current datetime

|

||||||

:param current_rate: Rate, calculated based on pricing settings in exit_pricing.

|

:param current_rate: Rate, calculated based on pricing settings in exit_pricing.

|

||||||

:param proposed_leverage: A leverage proposed by the bot.

|

:param proposed_leverage: A leverage proposed by the bot.

|

||||||

:param max_leverage: Max leverage allowed on this pair

|

:param max_leverage: Max leverage allowed on this pair

|

||||||

|

:param entry_tag: Optional entry_tag (buy_tag) if provided with the buy signal.

|

||||||

:param side: 'long' or 'short' - indicating the direction of the proposed trade

|

:param side: 'long' or 'short' - indicating the direction of the proposed trade

|

||||||

:return: A leverage amount, which is between 1.0 and max_leverage.

|

:return: A leverage amount, which is between 1.0 and max_leverage.

|

||||||

"""

|

"""

|

||||||

return 1.0

|

return 1.0

|

||||||

```

|

```

|

||||||

|

|

||||||

|

All profit calculations include leverage. Stoploss / ROI also include leverage in their calculation.

|

||||||

|

Defining a stoploss of 10% at 10x leverage would trigger the stoploss with a 1% move to the downside.

|

||||||

|

|

|

||||||

|

|

@ -199,7 +199,7 @@ New string argument `side` - which can be either `"long"` or `"short"`.

|

||||||

``` python hl_lines="4"

|

``` python hl_lines="4"

|

||||||

class AwesomeStrategy(IStrategy):

|

class AwesomeStrategy(IStrategy):

|

||||||

def custom_stake_amount(self, pair: str, current_time: datetime, current_rate: float,

|

def custom_stake_amount(self, pair: str, current_time: datetime, current_rate: float,

|

||||||

proposed_stake: float, min_stake: float, max_stake: float,

|

proposed_stake: float, min_stake: Optional[float], max_stake: float,

|

||||||

entry_tag: Optional[str], **kwargs) -> float:

|

entry_tag: Optional[str], **kwargs) -> float:

|

||||||

# ...

|

# ...

|

||||||

return proposed_stake

|

return proposed_stake

|

||||||

|

|

@ -208,7 +208,7 @@ class AwesomeStrategy(IStrategy):

|

||||||

``` python hl_lines="4"

|

``` python hl_lines="4"

|

||||||

class AwesomeStrategy(IStrategy):

|

class AwesomeStrategy(IStrategy):

|

||||||

def custom_stake_amount(self, pair: str, current_time: datetime, current_rate: float,

|

def custom_stake_amount(self, pair: str, current_time: datetime, current_rate: float,

|

||||||

proposed_stake: float, min_stake: float, max_stake: float,

|

proposed_stake: float, min_stake: Optional[float], max_stake: float,

|

||||||

entry_tag: Optional[str], side: str, **kwargs) -> float:

|

entry_tag: Optional[str], side: str, **kwargs) -> float:

|

||||||

# ...

|

# ...

|

||||||

return proposed_stake

|

return proposed_stake

|

||||||

|

|

|

||||||

|

|

@ -171,8 +171,8 @@ official commands. You can ask at any moment for help with `/help`.

|

||||||

| `/locks` | Show currently locked pairs.

|

| `/locks` | Show currently locked pairs.

|

||||||

| `/unlock <pair or lock_id>` | Remove the lock for this pair (or for this lock id).

|

| `/unlock <pair or lock_id>` | Remove the lock for this pair (or for this lock id).

|

||||||

| `/profit [<n>]` | Display a summary of your profit/loss from close trades and some stats about your performance, over the last n days (all trades by default)

|

| `/profit [<n>]` | Display a summary of your profit/loss from close trades and some stats about your performance, over the last n days (all trades by default)

|

||||||

| `/forceexit <trade_id>` | Instantly exits the given trade (Ignoring `minimum_roi`).

|

| `/forceexit <trade_id> | /fx <tradeid>` | Instantly exits the given trade (Ignoring `minimum_roi`).

|

||||||

| `/forceexit all` | Instantly exits all open trades (Ignoring `minimum_roi`).

|

| `/forceexit all | /fx all` | Instantly exits all open trades (Ignoring `minimum_roi`).

|

||||||

| `/fx` | alias for `/forceexit`

|

| `/fx` | alias for `/forceexit`

|

||||||

| `/forcelong <pair> [rate]` | Instantly buys the given pair. Rate is optional and only applies to limit orders. (`force_entry_enable` must be set to True)

|

| `/forcelong <pair> [rate]` | Instantly buys the given pair. Rate is optional and only applies to limit orders. (`force_entry_enable` must be set to True)

|

||||||

| `/forceshort <pair> [rate]` | Instantly shorts the given pair. Rate is optional and only applies to limit orders. This will only work on non-spot markets. (`force_entry_enable` must be set to True)

|

| `/forceshort <pair> [rate]` | Instantly shorts the given pair. Rate is optional and only applies to limit orders. This will only work on non-spot markets. (`force_entry_enable` must be set to True)

|

||||||

|

|

@ -270,10 +270,15 @@ Return a summary of your profit/loss and performance.

|

||||||

> **Latest Trade opened:** `2 minutes ago`

|

> **Latest Trade opened:** `2 minutes ago`

|

||||||

> **Avg. Duration:** `2:33:45`

|

> **Avg. Duration:** `2:33:45`

|

||||||

> **Best Performing:** `PAY/BTC: 50.23%`

|

> **Best Performing:** `PAY/BTC: 50.23%`

|

||||||

|

> **Trading volume:** `0.5 BTC`

|

||||||

|

> **Profit factor:** `1.04`

|

||||||

|

> **Max Drawdown:** `9.23% (0.01255 BTC)`

|

||||||

|

|

||||||

The relative profit of `1.2%` is the average profit per trade.

|

The relative profit of `1.2%` is the average profit per trade.

|

||||||

The relative profit of `15.2 Σ%` is be based on the starting capital - so in this case, the starting capital was `0.00485701 * 1.152 = 0.00738 BTC`.

|

The relative profit of `15.2 Σ%` is be based on the starting capital - so in this case, the starting capital was `0.00485701 * 1.152 = 0.00738 BTC`.

|

||||||

Starting capital is either taken from the `available_capital` setting, or calculated by using current wallet size - profits.

|

Starting capital is either taken from the `available_capital` setting, or calculated by using current wallet size - profits.

|

||||||

|

Profit Factor is calculated as gross profits / gross losses - and should serve as an overall metric for the strategy.

|

||||||

|

Max drawdown corresponds to the backtesting metric `Absolute Drawdown (Account)` - calculated as `(Absolute Drawdown) / (DrawdownHigh + startingBalance)`.

|

||||||

|

|

||||||

### /forceexit <trade_id>

|

### /forceexit <trade_id>

|

||||||

|

|

||||||

|

|

@ -281,6 +286,7 @@ Starting capital is either taken from the `available_capital` setting, or calcul

|

||||||

|

|

||||||

!!! Tip

|

!!! Tip

|

||||||

You can get a list of all open trades by calling `/forceexit` without parameter, which will show a list of buttons to simply exit a trade.

|

You can get a list of all open trades by calling `/forceexit` without parameter, which will show a list of buttons to simply exit a trade.

|

||||||

|

This command has an alias in `/fx` - which has the same capabilities, but is faster to type in "emergency" situations.

|

||||||

|

|

||||||

### /forcelong <pair> [rate] | /forceshort <pair> [rate]

|

### /forcelong <pair> [rate] | /forceshort <pair> [rate]

|

||||||

|

|

||||||

|

|

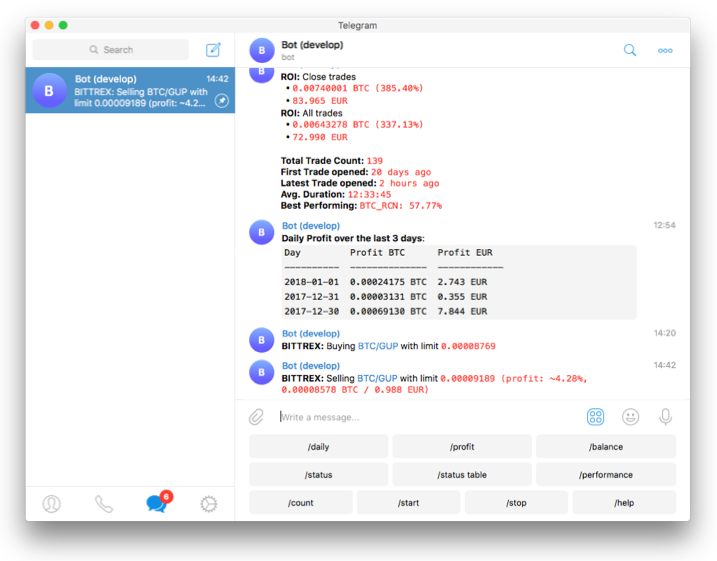

@ -328,11 +334,11 @@ Per default `/daily` will return the 7 last days. The example below if for `/dai

|

||||||

|

|

||||||

> **Daily Profit over the last 3 days:**

|

> **Daily Profit over the last 3 days:**

|

||||||

```

|

```

|

||||||

Day Profit BTC Profit USD

|

Day (count) USDT USD Profit %

|

||||||

---------- -------------- ------------

|

-------------- ------------ ---------- ----------

|

||||||

2018-01-03 0.00224175 BTC 29,142 USD

|

2022-06-11 (1) -0.746 USDT -0.75 USD -0.08%

|

||||||

2018-01-02 0.00033131 BTC 4,307 USD

|

2022-06-10 (0) 0 USDT 0.00 USD 0.00%

|

||||||

2018-01-01 0.00269130 BTC 34.986 USD

|

2022-06-09 (5) 20 USDT 20.10 USD 5.00%

|

||||||

```

|

```

|

||||||

|

|

||||||

### /weekly <n>

|

### /weekly <n>

|

||||||

|

|

@ -342,11 +348,11 @@ from Monday. The example below if for `/weekly 3`:

|

||||||

|

|

||||||

> **Weekly Profit over the last 3 weeks (starting from Monday):**

|

> **Weekly Profit over the last 3 weeks (starting from Monday):**

|

||||||

```

|

```

|

||||||

Monday Profit BTC Profit USD

|

Monday (count) Profit BTC Profit USD Profit %

|

||||||

---------- -------------- ------------

|

------------- -------------- ------------ ----------

|

||||||

2018-01-03 0.00224175 BTC 29,142 USD

|

2018-01-03 (5) 0.00224175 BTC 29,142 USD 4.98%

|

||||||

2017-12-27 0.00033131 BTC 4,307 USD

|

2017-12-27 (1) 0.00033131 BTC 4,307 USD 0.00%

|

||||||

2017-12-20 0.00269130 BTC 34.986 USD

|

2017-12-20 (4) 0.00269130 BTC 34.986 USD 5.12%

|

||||||

```

|

```

|

||||||

|

|

||||||

### /monthly <n>

|

### /monthly <n>

|

||||||

|

|

@ -356,11 +362,11 @@ if for `/monthly 3`:

|

||||||

|

|

||||||

> **Monthly Profit over the last 3 months:**

|

> **Monthly Profit over the last 3 months:**

|

||||||

```

|

```

|

||||||

Month Profit BTC Profit USD

|

Month (count) Profit BTC Profit USD Profit %

|

||||||

---------- -------------- ------------

|

------------- -------------- ------------ ----------

|

||||||

2018-01 0.00224175 BTC 29,142 USD

|

2018-01 (20) 0.00224175 BTC 29,142 USD 4.98%

|

||||||