16 KiB

Feature engineering

Defining the features

Low level feature engineering is performed in the user strategy within a function called populate_any_indicators(). That function sets the base features such as, RSI, MFI, EMA, SMA, time of day, volume, etc. The base features can be custom indicators or they can be imported from any technical-analysis library that you can find. One important syntax rule is that all base features string names are prepended with %-{pair}, while labels/targets are prepended with &.

!!! Note Adding the full pair string, e.g. XYZ/USD, in the feature name enables improved performance for dataframe caching on the backend. If you decide not to add the full pair string in the feature string, FreqAI will operate in a reduced performance mode.

Meanwhile, high level feature engineering is handled within "feature_parameters":{} in the FreqAI config. Within this file, it is possible to decide large scale feature expansions on top of the base_features such as "including correlated pairs" or "including informative timeframes" or even "including recent candles."

It is advisable to start from the template populate_any_indicators() in the source provided example strategy (found in templates/FreqaiExampleStrategy.py) to ensure that the feature definitions are following the correct conventions. Here is an example of how to set the indicators and labels in the strategy:

def populate_any_indicators(

self, pair, df, tf, informative=None, set_generalized_indicators=False

):

"""

Function designed to automatically generate, name, and merge features

from user-indicated timeframes in the configuration file. The user controls the indicators

passed to the training/prediction by prepending indicators with `'%-' + pair `

(see convention below). I.e., the user should not prepend any supporting metrics

(e.g., bb_lowerband below) with % unless they explicitly want to pass that metric to the

model.

:param pair: pair to be used as informative

:param df: strategy dataframe which will receive merges from informatives

:param tf: timeframe of the dataframe which will modify the feature names

:param informative: the dataframe associated with the informative pair

"""

if informative is None:

informative = self.dp.get_pair_dataframe(pair, tf)

# first loop is automatically duplicating indicators for time periods

for t in self.freqai_info["feature_parameters"]["indicator_periods_candles"]:

t = int(t)

informative[f"%-{pair}rsi-period_{t}"] = ta.RSI(informative, timeperiod=t)

informative[f"%-{pair}mfi-period_{t}"] = ta.MFI(informative, timeperiod=t)

informative[f"%-{pair}adx-period_{t}"] = ta.ADX(informative, window=t)

bollinger = qtpylib.bollinger_bands(

qtpylib.typical_price(informative), window=t, stds=2.2

)

informative[f"{pair}bb_lowerband-period_{t}"] = bollinger["lower"]

informative[f"{pair}bb_middleband-period_{t}"] = bollinger["mid"]

informative[f"{pair}bb_upperband-period_{t}"] = bollinger["upper"]

informative[f"%-{pair}bb_width-period_{t}"] = (

informative[f"{pair}bb_upperband-period_{t}"]

- informative[f"{pair}bb_lowerband-period_{t}"]

) / informative[f"{pair}bb_middleband-period_{t}"]

informative[f"%-{pair}close-bb_lower-period_{t}"] = (

informative["close"] / informative[f"{pair}bb_lowerband-period_{t}"]

)

informative[f"%-{pair}relative_volume-period_{t}"] = (

informative["volume"] / informative["volume"].rolling(t).mean()

)

indicators = [col for col in informative if col.startswith("%")]

# This loop duplicates and shifts all indicators to add a sense of recency to data

for n in range(self.freqai_info["feature_parameters"]["include_shifted_candles"] + 1):

if n == 0:

continue

informative_shift = informative[indicators].shift(n)

informative_shift = informative_shift.add_suffix("_shift-" + str(n))

informative = pd.concat((informative, informative_shift), axis=1)

df = merge_informative_pair(df, informative, self.config["timeframe"], tf, ffill=True)

skip_columns = [

(s + "_" + tf) for s in ["date", "open", "high", "low", "close", "volume"]

]

df = df.drop(columns=skip_columns)

# Add generalized indicators here (because in live, it will call this

# function to populate indicators during training). Notice how we ensure not to

# add them multiple times

if set_generalized_indicators:

df["%-day_of_week"] = (df["date"].dt.dayofweek + 1) / 7

df["%-hour_of_day"] = (df["date"].dt.hour + 1) / 25

# user adds targets here by prepending them with &- (see convention below)

# If user wishes to use multiple targets, a multioutput prediction model

# needs to be used such as templates/CatboostPredictionMultiModel.py

df["&-s_close"] = (

df["close"]

.shift(-self.freqai_info["feature_parameters"]["label_period_candles"])

.rolling(self.freqai_info["feature_parameters"]["label_period_candles"])

.mean()

/ df["close"]

- 1

)

return df

In the presented example, the user does not wish to pass the bb_lowerband as a feature to the model,

and has therefore not prepended it with %. The user does, however, wish to pass bb_width to the

model for training/prediction and has therefore prepended it with %.

After having defined the base features, the next step is to expand upon them using the powerful feature_parameters in the configuration file:

"freqai": {

//...

"feature_parameters" : {

"include_timeframes": ["5m","15m","4h"],

"include_corr_pairlist": [

"ETH/USD",

"LINK/USD",

"BNB/USD"

],

"label_period_candles": 24,

"include_shifted_candles": 2,

"indicator_periods_candles": [10, 20]

},

//...

}

The include_timeframes in the config above are the timeframes (tf) of each call to populate_any_indicators() in the strategy. In the presented case, the user is asking for the 5m, 15m, and 4h timeframes of the rsi, mfi, roc, and bb_width to be included in the feature set.

You can ask for each of the defined features to be included also for informative pairs using the include_corr_pairlist. This means that the feature set will include all the features from populate_any_indicators on all the include_timeframes for each of the correlated pairs defined in the config (ETH/USD, LINK/USD, and BNB/USD in the presented example).

include_shifted_candles indicates the number of previous candles to include in the feature set. For example, include_shifted_candles: 2 tells FreqAI to include the past 2 candles for each of the features in the feature set.

In total, the number of features the user of the presented example strat has created is: length of include_timeframes * no. features in populate_any_indicators() * length of include_corr_pairlist * no. include_shifted_candles * length of indicator_periods_candles

= 3 * 3 * 3 * 2 * 2 = 108.

Returning additional info from training

Important metrics can be returned to the strategy at the end of each model training by assigning them to dk.data['extra_returns_per_train']['my_new_value'] = XYZ inside the custom prediction model class.

FreqAI takes the my_new_value assigned in this dictionary and expands it to fit the dataframe that is returned to the strategy. You can then use the returned metrics in your strategy through dataframe['my_new_value']. An example of how return values can be used in FreqAI are the &*_mean and &*_std values that are used to created a dynamic target threshold.

Another example, where the user wants to use live metrics from the trade database, is shown below:

"freqai": {

"extra_returns_per_train": {"total_profit": 4}

}

You need to set the standard dictionary in the config so that FreqAI can return proper dataframe shapes. These values will likely be overridden by the prediction model, but in the case where the model has yet to set them, or needs a default initial value, the pre-set values are what will be returned.

Feature normalization

FreqAI is strict when it comes to data normalization. The train features, X^{train}, are always normalized to [-1, 1] using a shifted min-max normalization:

X^{train}_{norm} = 2 * \frac{X^{train} - X^{train}.min()}{X^{train}.max() - X^{train}.min()} - 1All other data (test data and unseen prediction data in dry/live/backtest) is always automatically normalized to the training feature space according to industry standards. FreqAI stores all the metadata required to ensure that test and prediction features will be properly normalized and that predictions are properly denormalized. For this reason, it is not recommended to eschew industry standards and modify FreqAI internals - however - advanced users can do so by inheriting train() in their custom IFreqaiModel and using their own normalization functions.

Data dimensionality reduction with Principal Component Analysis

You can reduce the dimensionality of your features by activating the principal_component_analysis in the config:

"freqai": {

"feature_parameters" : {

"principal_component_analysis": true

}

}

This will perform PCA on the features and reduce their dimensionality so that the explained variance of the data set is >= 0.999. Reducing data dimensionality makes training the model faster and hence allows for more up-to-date models.

Inlier metric

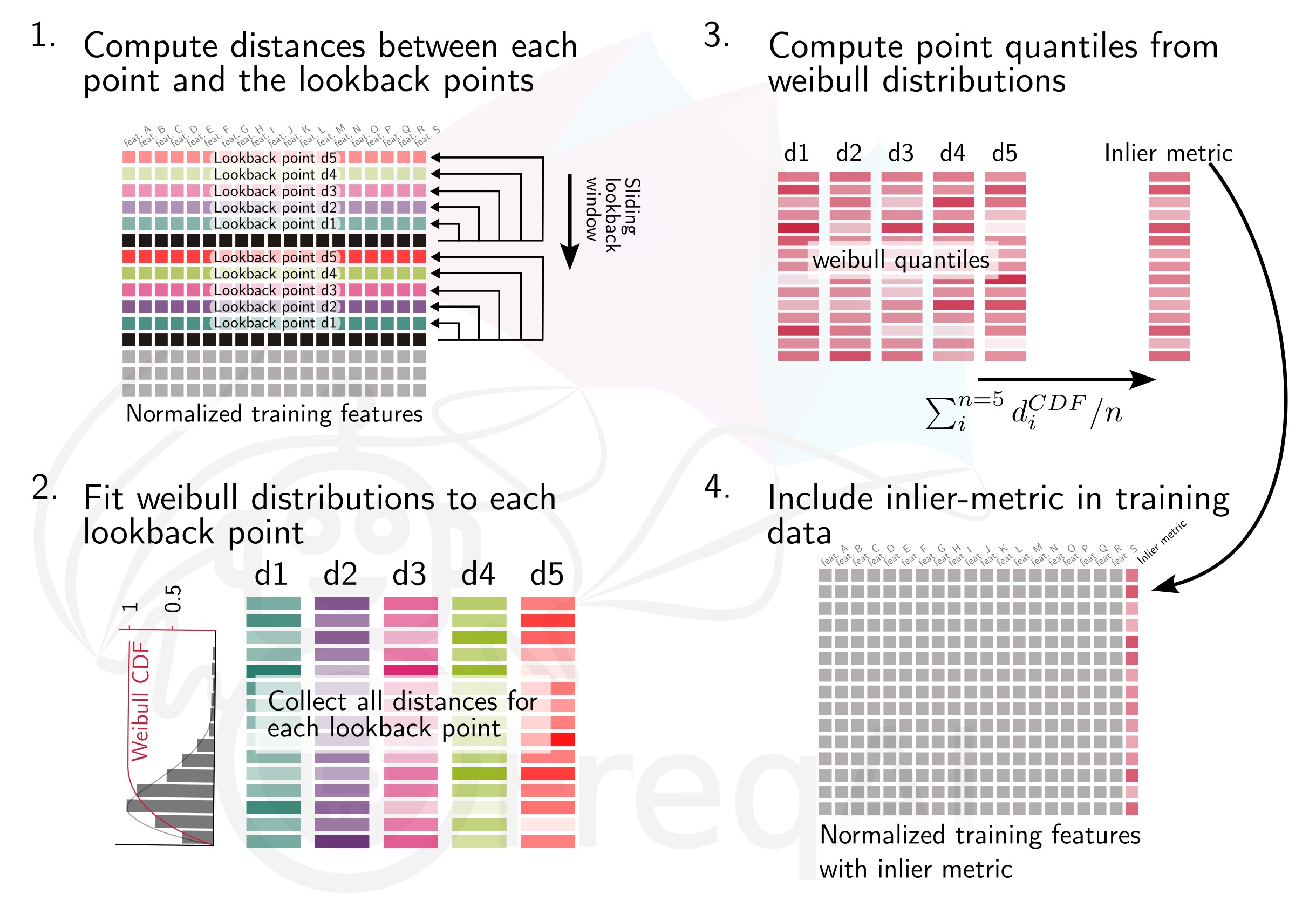

The inlier_metric is a metric aimed at quantifying how similar a the features of a data point are to the most recent historic data points.

You define the lookback window by setting inlier_metric_window and FreqAI computes the distance between the present time point and each of the previous inlier_metric_window lookback points. A Weibull function is fit to each of the lookback distributions and its cumulative distribution function (CDF) is used to produce a quantile for each lookback point. The inlier_metric is then computed for each time point as the average of the corresponding lookback quantiles. The figure below explains the concept for an inlier_metric_window of 5.

FreqAI adds the inlier_metric to the training features and hence gives the model access to a novel type of temporal information.

This function does not remove outliers from the data set.

Weighting features for temporal importance

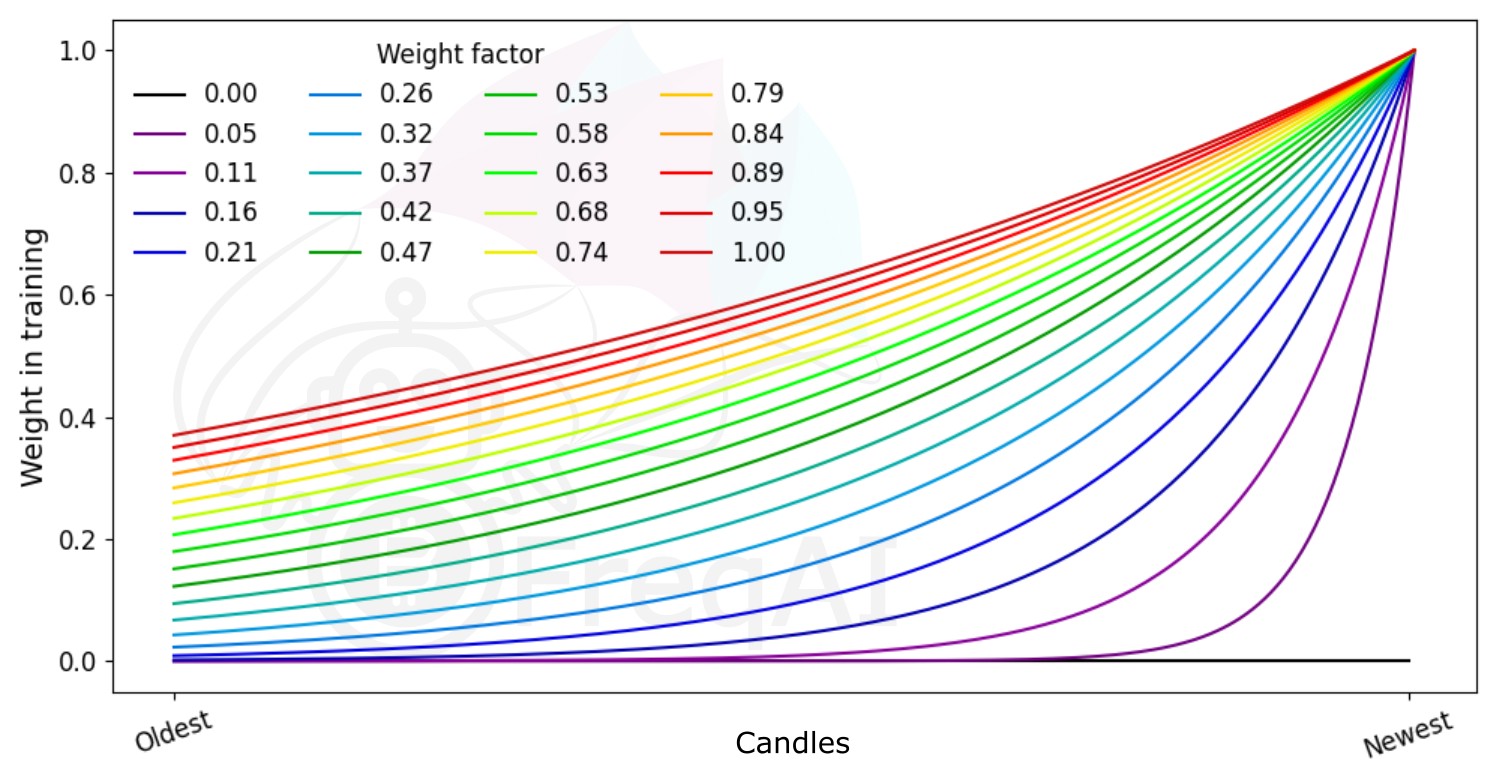

FreqAI allows you to set a weight_factor to weight recent data more strongly than past data via an exponential function:

W_i = \exp(\frac{-i}{\alpha*n}) where W_i is the weight of data point i in a total set of n data points. Below is a figure showing the effect of different weight factors on the data points in a feature set.

Outlier detection

Equity and crypto markets suffer from a high level of non-patterned noise in the form of outlier data points. FreqAI implements a variety of methods to identify such outliers and hence mitigate risk.

Identifying outliers with the Dissimilarity Index (DI)

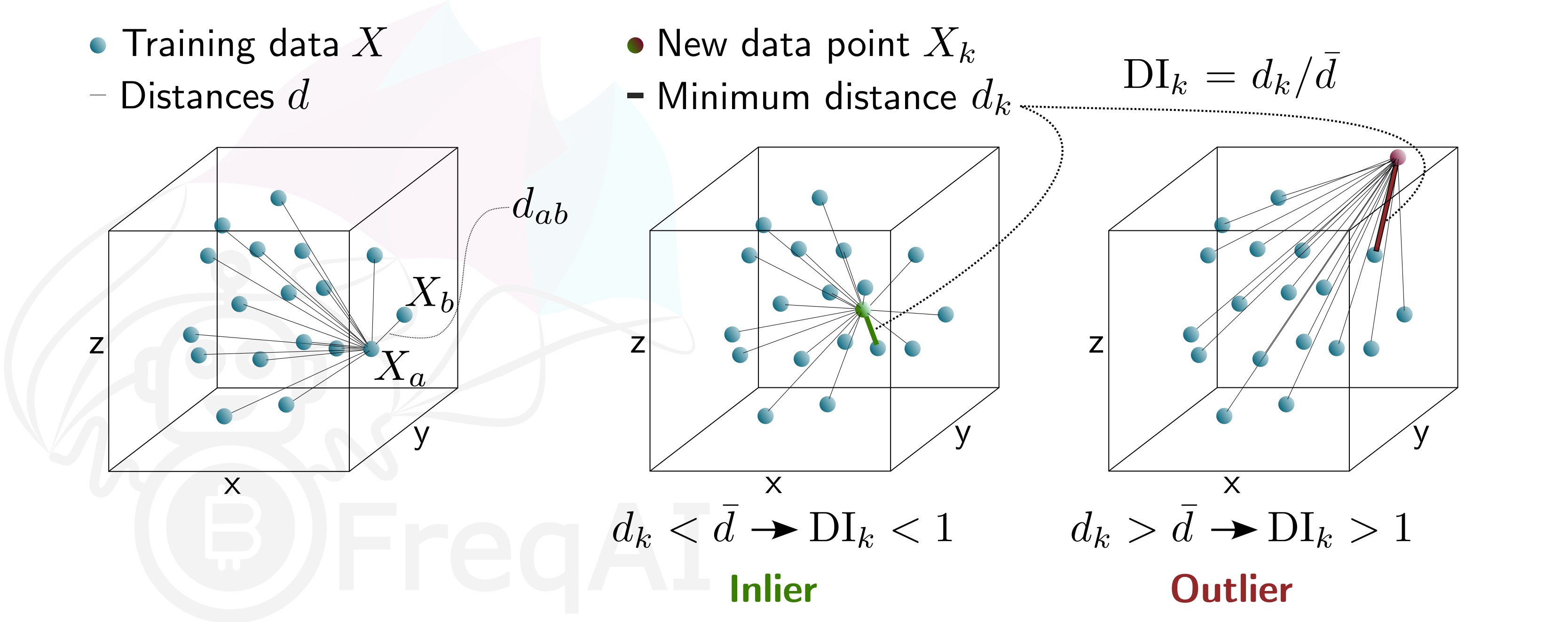

The Dissimilarity Index (DI) aims to quantify the uncertainty associated with each prediction made by the model.

You can tell FreqAI to remove outlier data points from the training/test data sets using the DI by including the following statement in the config:

"freqai": {

"feature_parameters" : {

"DI_threshold": 1

}

}

The DI allows predictions which are outliers (not existent in the model feature space) to be thrown out due to low levels of certainty. To do so, FreqAI measures the distance between each training data point (feature vector), X_{a}, and all other training data points:

d_{ab} = \sqrt{\sum_{j=1}^p(X_{a,j}-X_{b,j})^2} where d_{ab} is the distance between the normalized points a and b, and p is the number of features, i.e., the length of the vector X. The characteristic distance, \overline{d}, for a set of training data points is simply the mean of the average distances:

\overline{d} = \sum_{a=1}^n(\sum_{b=1}^n(d_{ab}/n)/n) \overline{d} quantifies the spread of the training data, which is compared to the distance between a new prediction feature vectors, X_k and all the training data:

d_k = \arg \min d_{k,i} This enables the estimation of the Dissimilarity Index as:

DI_k = d_k/\overline{d} You can tweak the DI through the DI_threshold to increase or decrease the extrapolation of the trained model. A higher DI_threshold means that the DI is more lenient and allows predictions further away from the training data to be used whilst a lower DI_threshold has the opposite effect and hence discards more predictions.

Below is a figure that describes the DI for a 3D data set.

Identifying outliers using a Support Vector Machine (SVM)

You can tell FreqAI to remove outlier data points from the training/test data sets using a Support Vector Machine (SVM) by including the following statement in the config:

"freqai": {

"feature_parameters" : {

"use_SVM_to_remove_outliers": true

}

}

The SVM will be trained on the training data and any data point that the SVM deems to be beyond the feature space will be removed.

FreqAI uses sklearn.linear_model.SGDOneClassSVM (details are available on scikit-learn's webpage here (external website)) and you can elect to provide additional parameters for the SVM, such as shuffle, and nu.

The parameter shuffle is by default set to False to ensure consistent results. If it is set to True, running the SVM multiple times on the same data set might result in different outcomes due to max_iter being to low for the algorithm to reach the demanded tol. Increasing max_iter solves this issue but causes the procedure to take longer time.

The parameter nu, very broadly, is the amount of data points that should be considered outliers and should be between 0 and 1.

Identifying outliers with DBSCAN

You can configure FreqAI to use DBSCAN to cluster and remove outliers from the training/test data set or incoming outliers from predictions, by activating use_DBSCAN_to_remove_outliers in the config:

"freqai": {

"feature_parameters" : {

"use_DBSCAN_to_remove_outliers": true

}

}

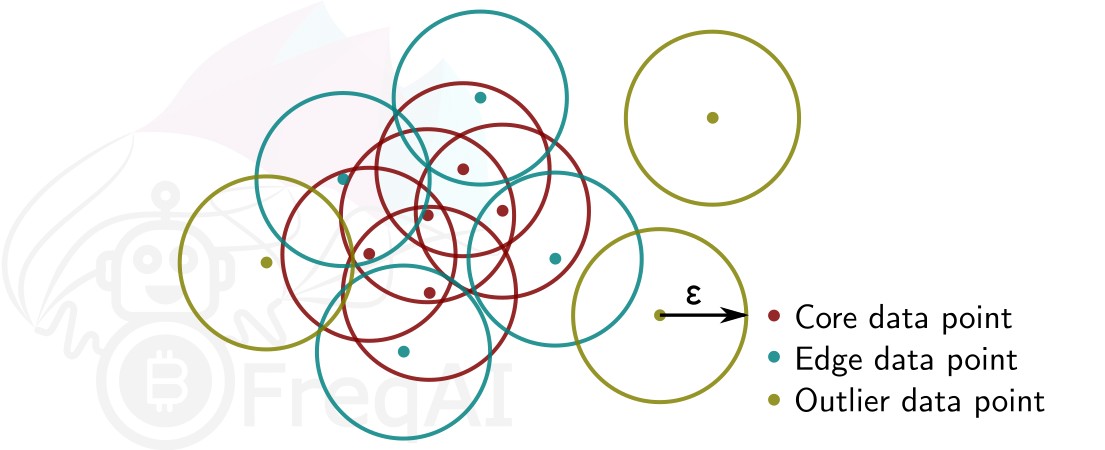

DBSCAN is an unsupervised machine learning algorithm that clusters data without needing to know how many clusters there should be.

Given a number of data points N, and a distance \varepsilon, DBSCAN clusters the data set by setting all data points that have N-1 other data points within a distance of \varepsilon as core points. A data point that is within a distance of \varepsilon from a core point but that does not have N-1 other data points within a distance of \varepsilon from itself is considered an edge point. A cluster is then the collection of core points and edge points. Data points that have no other data points at a distance <\varepsilon are considered outliers. The figure below shows a cluster with N = 3.

FreqAI uses sklearn.cluster.DBSCAN (details are available on scikit-learn's webpage here (external website)) with min_samples ($N$) taken as 1/4 of the no. of time points (candles) in the feature set. eps ($\varepsilon$) is computed automatically as the elbow point in the k-distance graph computed from the nearest neighbors in the pairwise distances of all data points in the feature set.